Five key takeaways

- DeFi yields are transitioning from token rewards to sustainable, fee-driven revenue models, surpassing $6B in fees earned in 2024.

- Onchain lending is flourishing from higher borrowing demand, with USD yields averaging ~10%, far outpacing TradFi returns.

- Bridging and staking are safer than ever, with stronger risk management making them foundational elements of DeFi.

- Bitcoin staking could unlock $100B in idle capital, potentially increasing DeFi TVL by over 50%.

- Innovations like restaking, perpetual DEXs, and real-world assets are rebalancing DeFi’s tradeoffs, unlocking more efficient ways to generate yield and scale the ecosystem.

Introduction

DeFi has transcended its incentive-driven origins, evolving into an ecosystem where real utility and sustainable fee models are taking center stage. While critics like Vitalik Buterin have labeled DeFi an ouroboros — dependent on the perpetual motion of crypto trading — this view overlooks the sector’s steady progression toward sustainability.

In 2024, 77% of DeFi yields came from real fee revenues — a notable improvement from the reward — heavy emissions of the past. Yes, trading volumes still contribute to this, but a growing share stems from services that address tangible demands: stablecoin transactions for remittances, lending and borrowing for actual liquidity needs, decentralised derivatives trading for hedging, and the tokenization of real-world assets. It’s a sign of a maturing industry, one whose revenue is rooted in providing actual utility rather than relying solely on token incentives or speculative fervor.

DeFi’s maturation is further highlighted by the $6B in yield earned by liquidity providers in 2024, a testament to the ecosystem’s ability to generate real cash flows. This growth has been driven by its foundational pillars, which include staking, lending, market making, and bridging, and they provide critical infrastructure for capital efficiency, liquidity, and interoperability. These are bona fide financial services delivered onchain, enabling DeFi to emerge as a cornerstone of the global financial system.

With momentum accelerating across the ecosystem, DeFi is proving its ability to scale sustainably and attract capital from both retail and institutional investors. The questions of yesterday — about risk, decentralisation, and economic design — are giving way to a new era of growth and innovation. What follows is a closer look at the forces driving this evolution and the opportunities that lie ahead for DeFi to reach even greater heights.

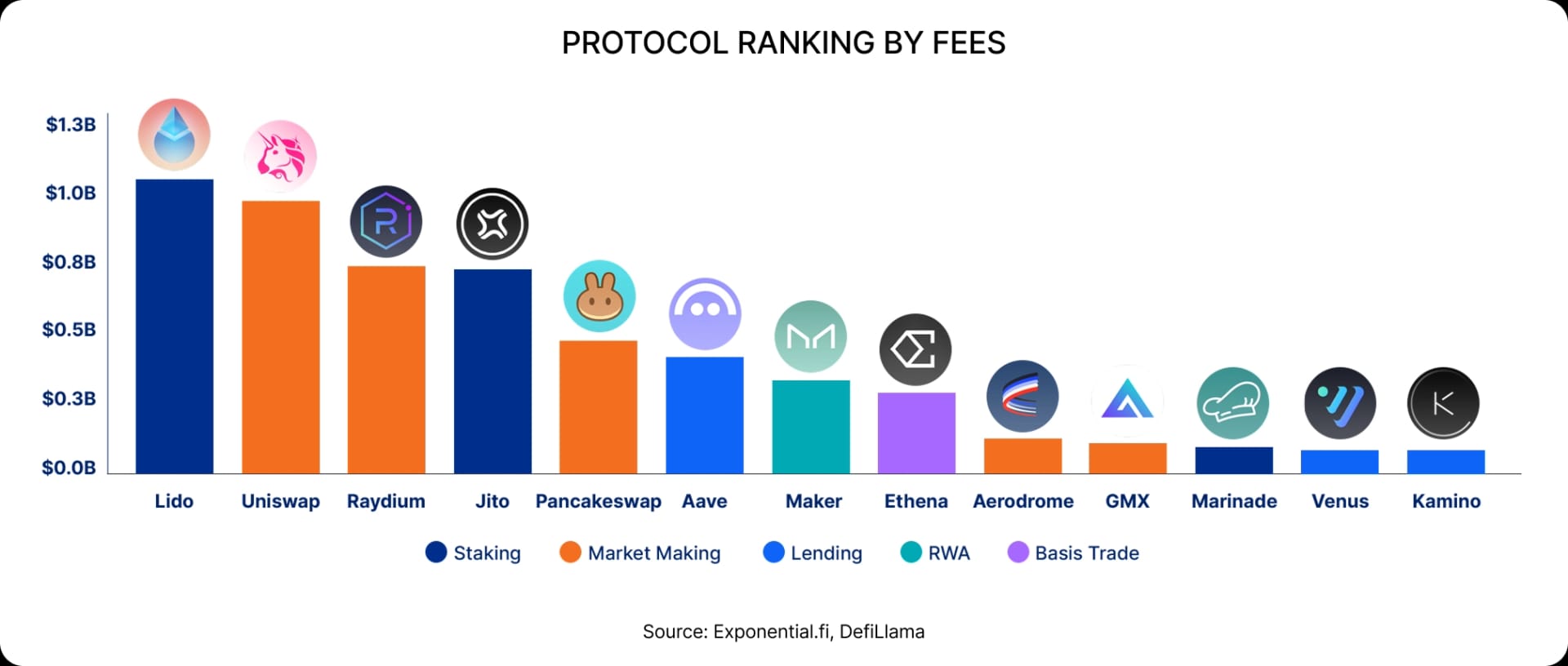

DeFi yields are transitioning from token rewards to sustainable, fee- driven revenue models, surpassing $6B in fees earned in 2024

In the early days of DeFi, protocols relied heavily on token rewards to bootstrap liquidity and attract users. While effective initially, this approach often resulted in unsustainable emissions, diluting token value and creating fleeting incentives. Over the past year, however, DeFi has seen a meaningful shift toward more sustainable, fee-driven yield models, reflecting the ecosystem’s growing maturity.

This transition aligns with broader market trends as users prioritize yield sustainability and protocols compete on efficiency rather than emissions. Protocols like Lido, Uniswap, and Aave have demonstrated that real, fee-based revenues are not only achievable but are becoming the foundation of DeFi’s yield generation. Across all DeFi protocols, total fees earned by liquidity providers in 2024 surpassed $6B. DeFi’s total market cap reached $130B in 2024, which positions the sector at an approximate 20x P/E multiple — a compelling valuation for a rapidly growing industry that continues to outpace traditional finance in innovation and adoption.

Lending protocols, for example, now generate the majority of their yields from borrow rates rather than token incentives. Similarly, decentralised exchanges (DEXs) like Uniswap continue to generate substantial trading fees for liquidity providers without any incentives. In the staking sector, liquid staking tokens (LSTs) provide stakers with staking rewards from protocol emissions, gas fees, and MEV sharing.

The shift away from rewards has also reduced systemic risk. High token emissions often encouraged “hot money,” which would flow rapidly in and out of protocols, increasing volatility and vulnerability.

By transitioning to fee-driven models, DeFi is attracting more stable capital, reinforcing the long-term health of the ecosystem.

As DeFi continues to evolve, the reliance on token rewards will likely diminish further and be replaced by scalable, user-driven revenue. This trend not only enhances protocol sustainability but also makes DeFi yields more attractive to institutional investors, who increasingly view the sector as a viable alternative to traditional financial instruments.

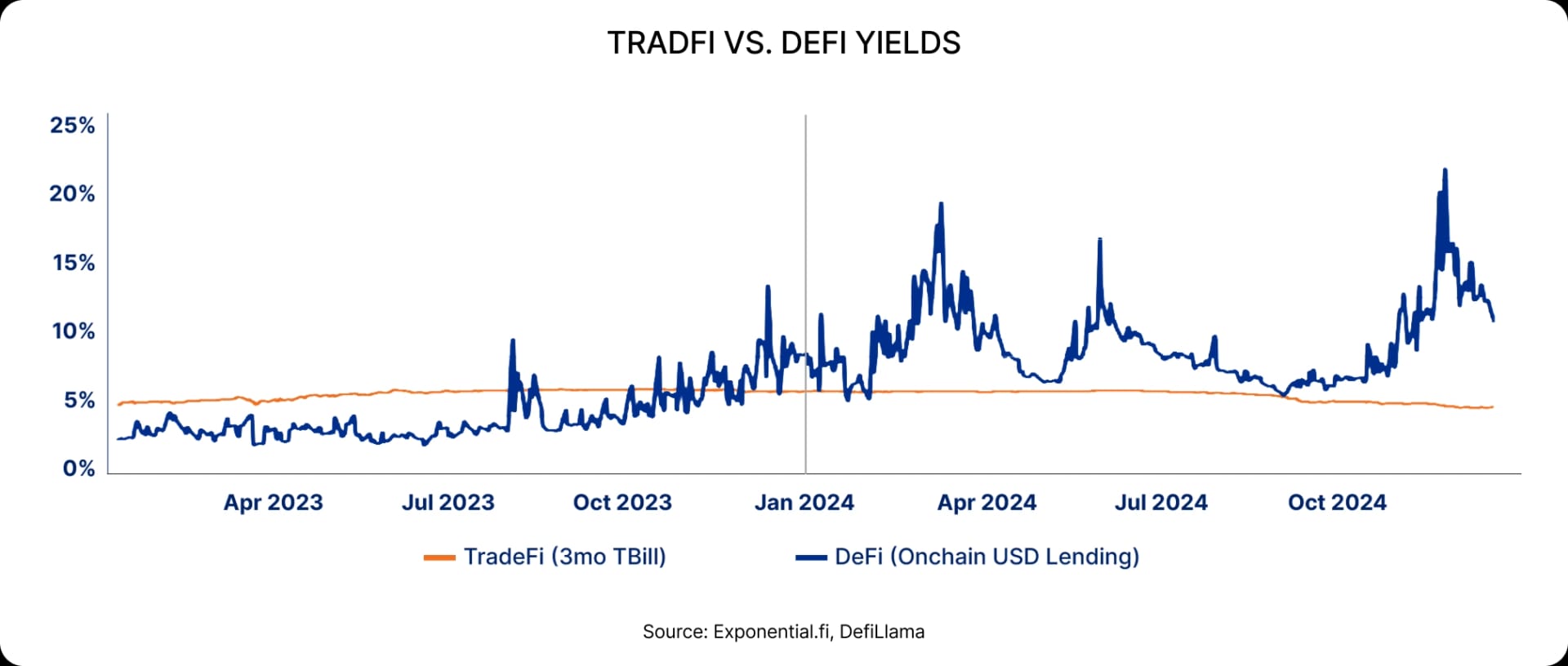

Onchain lending is flourishing from higher borrowing demand, with USD yields averaging ~10%, far outpacing TradFi returns

The onchain lending market reached new milestones in 2024, with total value locked (TVL) in lending protocols surpassing $54.1B — an all-time high and a 139% increase from 2023. This growth has been fueled by a combination of rising yields, increasing demand for leverage in crypto markets, and improvements in risk management that have made DeFi lending more secure and accessible.

Borrowing activity surged during the year, particularly in Q4, driving significant earnings for lenders. Aave, the dominant lending protocol, led this expansion, with outstanding borrows increasing over 4x, from $3.4B to $14.5B by year-end. Over the same period, Aave more than doubled its user base to around 60,000 unique borrowers. Borrow rates in Aave’s USDC market climbed from 6% APY at the start of the year to a peak of 17% during the Q4 rally, before stabilizing around 10%.

Morpho, a rising star in the lending sector, has gained traction with its innovative approach to risk management. By combining isolated lending vaults, an immutable design, and risk curation, Morpho delivers tailored solutions for niche assets, reducing systemic risk while attracting a growing user base. In 2024, outstanding borrows on the platform surged from under $814M to over $2B, generating $57M in interest for lenders by year-end. This remarkable growth highlights the increasing demand for secure, efficient lending models in DeFi that balance yield generation with risk mitigation.

DeFi lending yields are increasingly competitive with traditional finance returns, particularly as recent changes to central bank policies have pressured cash savings rates. While TradFi yields declined in the second half of 2024, onchain lending yields consistently exceeded 10% across top protocols, driven by heightened borrowing demand. This yield premium is making DeFi an attractive option for yield-seeking investors and further accelerating adoption among both retail and institutional users.

Improved risk management has also played a critical role in the sector’s growth. Protocols like Aave have maintained their reputation for security, avoiding major exploits and implementing features like isolated markets to manage risk more effectively. The maturation of lending protocols has reduced systemic vulnerabilities and reassured users, contributing to the steady inflow of capital into DeFi lending pools.

The increasing gap between DeFi and TradFi yields underscores a broader trend: onchain lending is no longer just a niche product but a compelling alternative to traditional financial instruments. With borrowing demand remaining strong and protocols continuously improving efficiency and security, DeFi lending is positioned to attract even more capital in 2025.

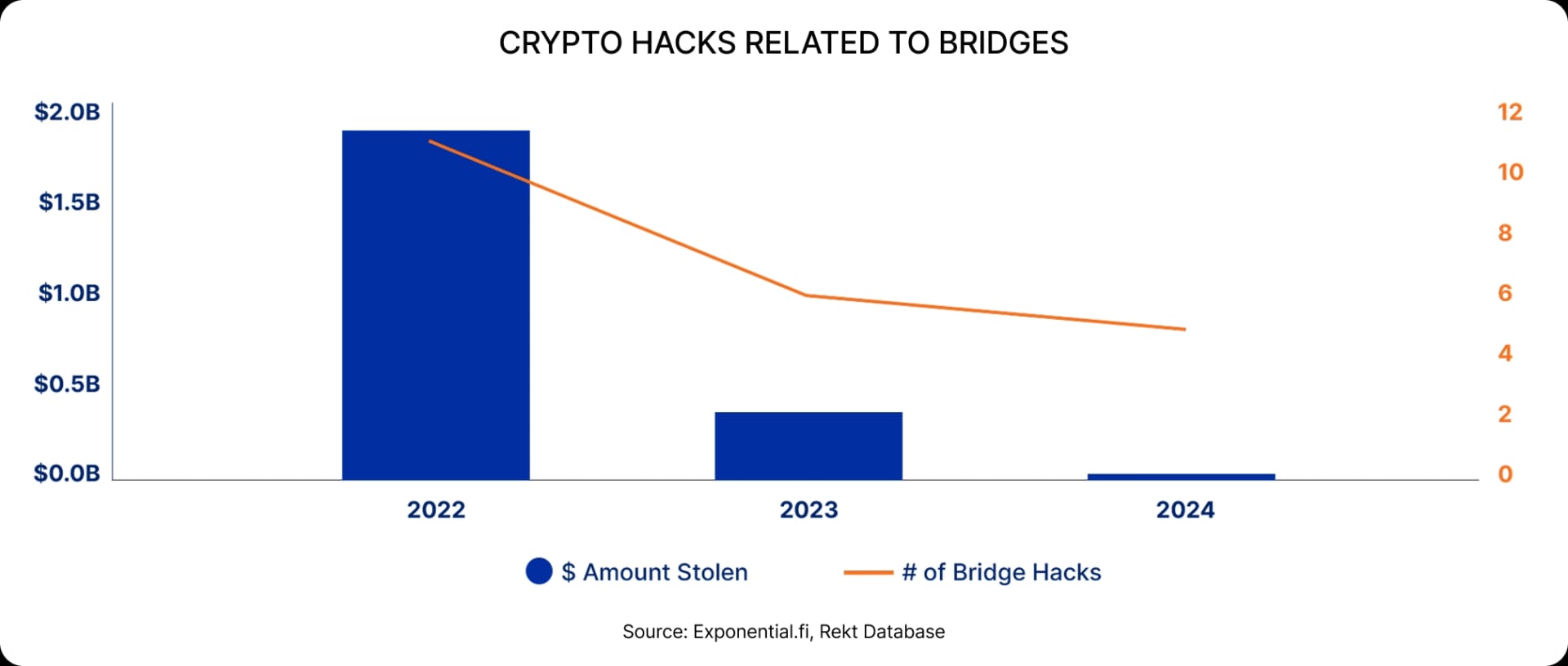

Bridging and staking are safer than ever, with stronger risk management making them foundational elements of DeFi

The bridging sector, once notorious for high-profile exploits, experienced a dramatic decline in security incidents. Losses from bridge hacks dropped by over 95% year-over-year, with only $19M in funds compromised. This dramatic reduction reflects the sector’s growing maturity and its ability to address long-standing vulnerabilities, restoring confidence in cross-chain infrastructure.

Meanwhile, bridging total value locked (TVL) climbed to $50.7B by December, highlighting sustained demand for cross-chain liquidity. Innovations like intent-based mechanisms and native token bridging solutions have played a pivotal role in reducing risk and improving the user experience in cross-chain interactions.

Intent-based mechanisms shift execution risks from users to solvers by allowing users to specify their desired outcomes, such as transferring tokens to another chain, without managing the underlying processes. Solvers, operating within a competitive auction framework, handle execution, ensuring transactions are both efficient and secure. This design minimises user exposure to transaction failures or vulnerabilities, as solvers bear the responsibility for execution risks.

Native token bridging solutions, such as Circle’s Cross-Chain Transfer Protocol (CCTP), further enhance security by eliminating the need for wrapped tokens. Instead of locking assets on one chain and minting a wrapped version on another, these solutions use mechanisms like burn-and- mint, where tokens are burned on the source chain and freshly minted on the destination chain. By bypassing the need to hold large reserves of locked assets in bridge contracts — a common feature of many DeFi bridges — this approach significantly reduces the large, exploitable honeypots that have historically been targeted in bridge hacks.

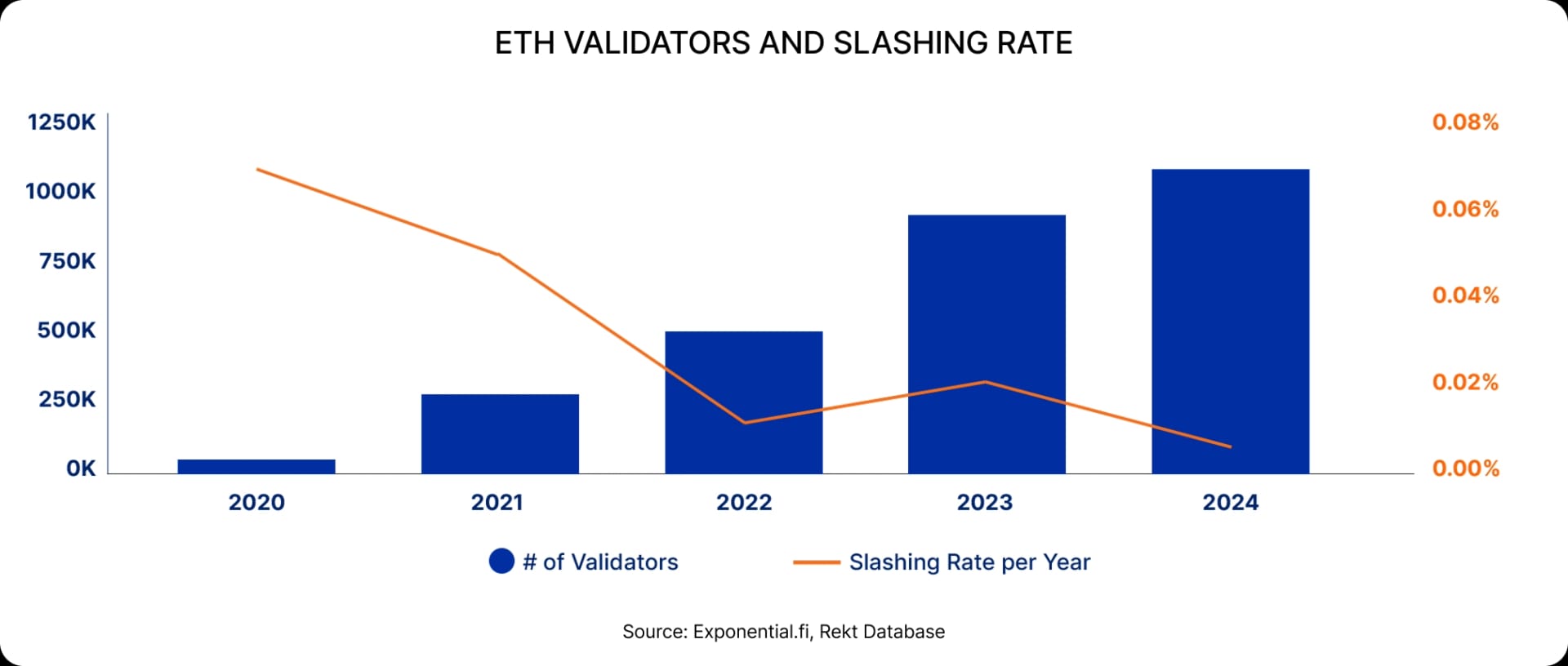

Similarly, staking has solidified its position as the backbone of blockchain network security, with Ethereum leading the way after its successful transition to Proof-of-Stake (PoS). Staking TVL reached new heights in 2024, driven by Ethereum’s growing participation rate, which doubled to 28% following the Shapella upgrade. Liquid Staking Tokens (LSTs) played a crucial role in this growth, offering users the ability to stake assets while maintaining liquidity.

Despite concerns about slashing risks, the data shows these incidents remain exceedingly rare. For example, less than 0.04% of ETH validators have been slashed since the launch of Ethereum’s Beacon Chain in December 2020, with only 0.01% slashed in 2024, underscoring the reliability of modern staking protocols.

Innovations like Distributed Validator Technology (DVT) have further strengthened the security of staking pools by decentralising validator responsibilities across multiple operators. This approach reduces the likelihood of slashing caused by downtime or operator errors, providing an added layer of protection for stakers.

As bridging becomes more efficient and staking more accessible, these two sectors are cementing their roles as pillars of the DeFi ecosystem. The reduced exploit rates in bridging and the growing resilience of staking demonstrate how far DeFi has come in addressing its early vulnerabilities. With continued innovation, these components will remain central to the expansion of DeFi.